Message from the President

The Arrival of the Black Ships: Suruga’s Point of Origin

This year marks the 130th anniversary of Suruga Bank, founded in 1895 by our first president, Kitaro Okano, under its original name, Negata Bank. As we reach this milestone in fiscal 2025, I am reminded once again of the weight of our history and the social responsibility that comes with it.

Suruga Bank’s roots trace back even earlier, to the arrival of the “Black Ships” in Japan. In 1853, Commodore Perry led a fleet of American naval vessels into Uraga Harbor. The following year, the Treaty of Peace and Amity between Japan and the United States was signed, setting Japan on a path to opening its doors to the world. In 1856, the first U.S. consul general was established in Shimoda, one of Japan’s first open ports.

Upon hearing this news, Yaheita Okano—father of our founder, Kitaro—hurried to Shimoda. Driven by the conviction that “a new Japan will begin here,” he threw himself into the heart of change, determined to witness Japan’s transformation firsthand. Fueled by passion and curiosity, he persuaded the local magistrate to let him live and work there.

While many people at the time likely saw the arrival of the Black Ships as a threat, Yaheita saw things differently. He had the mindset to embrace change, not as something to be feared, but as something exciting. He had the ambition to dive into change and turn it into opportunity. I believe that spirit, his DNA, lives on today in Suruga Bank’s commitment to taking on unprecedented challenges and creating “difference” as a core management philosophy.

Our corporate philosophy is to be a company that makes customers feel, “I’m glad you’re here... I’m glad we met.” Even with standard service delivered sincerely and attentively, we may still inspire the first kind of sentiment—gratitude that we are “here.” But to reach the level where customers truly feel grateful for the encounter itself, we must go further. We must continue to seek out and deliver new values, new products and services, and new ways of engaging with people that have never existed before. This steady, genuine commitment to creating “difference” for our customers has taken root throughout our organization, hand in hand with our corporate philosophy. In an era where change is accelerating, I hope to see more and more of our people enjoy transforming themselves and rising to new challenges. If that happens, I believe we will arrive at the future beyond a brighter Suruga—five or ten years from now.

In Times of Uncertainty, We Must Be Willing to Take Risks and Step Forward

If I had to describe the current business environment in a single word, it would be “uncertain.” From developments in the United States to the rise of geopolitical risks, economic fragmentation, and the spread of populism, the world is seeing a wave of events that defy past norms and values. As a result, it has become extremely difficult to predict where things are headed.

In such uncertain times, the financial industry is likely among the first to feel the impact. In the regional banking sector, for example, we are witnessing a wave of restructuring that differs significantly from the past. Previously, consolidations were often guided by regulatory authorities with a focus on rescuing weaker institutions. But today, we have entered a new era, one in which each bank must take the initiative to chart its own path forward. It is essential that we update our mindset to reflect this shift.

Amid this uncertainty, we are increasingly hearing concerns from our local corporate clients in Shizuoka and Kanagawa. While the local economy is gradually recovering and overall business conditions are not particularly bad, some clients remain hesitant—unsure whether now is the right time to increase investment and move forward. Deciding whether to take a risk and press ahead or to hold back is not an easy choice, even for us.

That said, if we return to Suruga Bank’s origins, it is precisely because times are uncertain that we should take the risk and step forward in what we believe is the right direction. The same was true when the Black Ships arrived. There was no way of knowing whether Commodore Perry’s fleet was friend or foe. And yet, looking back, their arrival marked a major turning point in Japan’s opening to the world. By engaging with them and understanding their thinking, Japan might have learned new things and adapted more quickly to change.

Remaining still can be just as risky as moving forward. Even when visibility is poor, we must not wait for the fog to lift. Instead, we should look for openings, see what lies ahead, and turn uncertainty into opportunity. This is the message I want to convey to both our employees and our customers.

Stronger-than-Expected Performance Set to Continue into Fiscal 2025

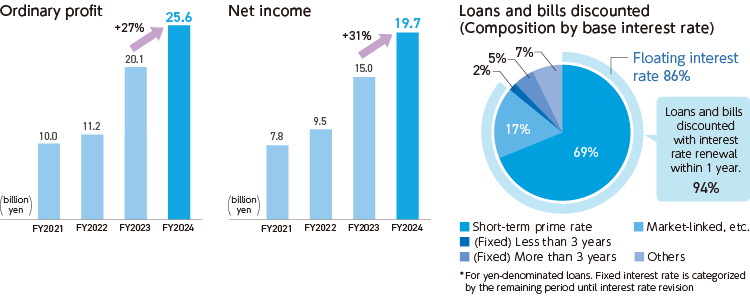

Fiscal 2024, the second year of our Mid-Term Management Plan Phase II (covering FY2023 to FY2025), marked our third consecutive year of profit growth. Compared to the previous year on a non-consolidated basis, ordinary profit rose by 27% and net income by 31%, exceeding expectations and reflecting strong business performance.

Notably, the impact of rising interest rates has not been fully reflected in our FY2024 results. Although 94% of our variable-rate loans are due for rate revision within one year—a high proportion—the full-scale positive effect on earnings is expected to materialize from fiscal 2025 onward.

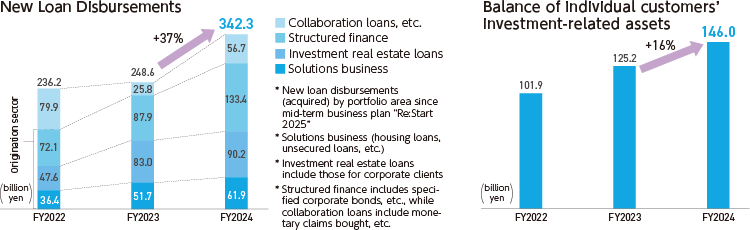

The strong performance was primarily driven by steady progress in both our loan business and asset consulting services. New loan origination continued to grow, with a year-on-year increase of 37% in fiscal 2024. In the asset consulting segment, the balance of individual customers’ investment-related assets under custody rose by 16%.

Underlying these solid results is our ongoing shift from the “Mt. Fuji Model” to the “Yatsugatake Model”—that is, from a single-peak structure to a diversified business model with multiple growth engines. Each of the four autonomous profit centers—Community Banking, Direct Banking, Greater Tokyo/Wide Area Banking, and Market Finance Division—has been led by a general manager who operates with a strong sense of ownership, as if running an independent company. Their autonomous decision-making and proactive leadership have played a key role in driving our strong performance.

Let me share an episode that illustrates how our profit center model is working in practice. At the Greater Tokyo/Wide Regional Banking division, a limited-time campaign drew far more interest than anticipated, resulting in a surge of work that nearly overwhelmed the team. Realizing that they couldn’t handle the volume alone, the person in charge brought the issue directly to the general manager, who coordinated the temporary transfer of staff from other departments to help. Thanks to this quick response, the team was able to manage the situation successfully. The departments that lent personnel may have experienced some negative impact on their own performance. Even so, they prioritized the overall optimization of the profit center and stepped in to solve the problem on their own initiative. I am deeply grateful for their proactive mindset and strong sense of autonomy.

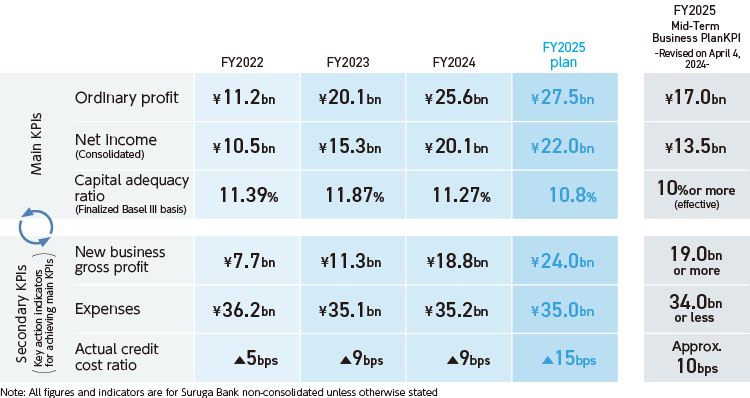

We expect this strong performance to continue into fiscal 2025. While it is the final year of our current Mid-Term Management Plan, we anticipate surpassing all of our KPIs, except for expenses. We are projecting ordinary profit of ¥27.5 billion, which would exceed the KPI target by ¥10.5 billion, or 61%. In terms of gross profit from new businesses, which reflects earnings from our new portfolio, we are forecasting ¥24.0 billion—¥5.0 billion above the KPI target of ¥19.0 billion. These figures clearly indicate that our V-shaped recovery and path to regrowth are firmly taking shape.

When we formulated our current Mid-Term Management Plan three years ago, I consistently conveyed a message to our employees that “Suruga’s future is bright.” At the time, I sensed that some staff were feeling uncertain about what lay ahead, so I deliberately chose to express a sense of optimism. Today, I believe that the majority of our employees genuinely share that conviction—that Suruga’s future is bright. With that in mind, I’ve recently updated the message to one that says “Let’s go beyond ‘bright’—toward a future filled with excitement.”

The word “bright” carries a somewhat passive nuance, as if it depends on favorable external conditions. In contrast, “excitement” is active—it arises when we commit ourselves to something, feel a sense of purpose, and find joy, fulfillment, or gratitude from our customers in return. I sincerely hope to make Suruga not only a “bright” company, but one that is exciting and fulfilling for everyone involved.

Strengthening Our Growth Engines to Maintain ROE of 8% or Above

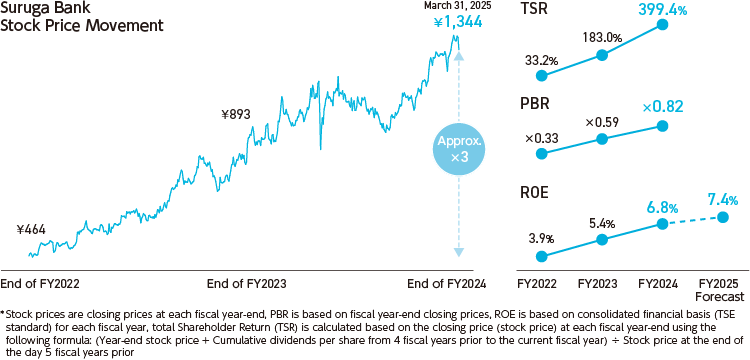

Our share price has approximately tripled over the two years from April 2023, when our Mid-Term Management Plan began, to the end of March 2025, reaching ¥1,344. For fiscal 2024, our five-year total shareholder return (TSR) stood at 399.4%, our price-to-book ratio (PBR) rose to 0.82x, and our return on equity (ROE) climbed to 6.8%. We believe these strong results reflect the steady progress of the various initiatives outlined in our Mid-Term Management Plan, and the positive assessment we’ve received from investors.

That said, a closer look reveals that our relatively strong share price and PBR compared to other regional banks are largely driven by price-to-earnings ratio (PER)—in other words, by expectations for future growth. To achieve further share price appreciation and a PBR exceeding 1.0x, we recognize that we must raise our ROE even further in a more fundamental and sustainable way.

Last year, we announced our target of maintaining an average ROE of 6% or over from fiscal 2026 onward, with a longer-term goal of 8% or over. For fiscal 2025, we are projecting ROE of 7.4%, just shy of what we consider the minimum passing threshold. However, in order to consistently achieve ROE 8% or above, it is not enough to focus solely on measures such as for the dividend payout ratio, executing share buybacks, or reducing cross-shareholdings. What matters most is strengthening the individual growth engines of our “Yatsugatake Model.” In that sense, we believe our efforts to enhance corporate value are still a work in progress.

While institutional investors have expressed appreciation for the initiatives we’ve undertaken over the past two years, we are increasingly being asked to show what comes next—our next stage of growth. Expectations for Suruga had fallen significantly at one point, but as we now make a solid V-shaped recovery, the question is how we plan to build on this momentum. Although we do not yet have a definitive answer, we aim to present a clear vision in our next Mid-Term Management Plan, which we intend to formulate during fiscal 2025.

Fiscal 2025 Management Policies: “PIVOT,” Strategic Investment in People, AI, and the Local Community, and a Future Beyond a Brighter Suruga

As fiscal 2025 marks the final year of our current Mid-Term Management Plan, we have established three key management policies.

The first is “PIVOT – Refining the Creation of Difference.” While “pivot” typically refers to a change in direction, we use the term to mean shifting one’s perspective or approach while keeping a firm footing—recognizing our core strengths and, from that stable foundation, adjusting our angle or line of sight to discover new ways of doing things.

One example of this pivot is the establishment of our Wealth Advisory Department in April 2025—an initiative proposed by employees targeting ultra-high-net-worth individuals. When such clients consider purchasing investment real estate, their primary focus is usually on the property itself. Whether they use a loan or which financial institution they choose often comes later. As a result, financial institutions have traditionally focused their sales efforts on real estate agents.

The Wealth Advisory Department takes a different approach by engaging directly with end users, bypassing real estate agents. Its main activities involve working with clients who have previously taken out real estate loans with us, those referred by private banks or other customers, and individuals who contact us directly. By applying the knowledge and expertise we have built up over many years—while shifting our perspective to create “difference”—we are uncovering new sources of demand.

The second policy is “Proactive Investment in People, AI, and the Local Community.” While we continue to pursue cost structure reforms, we are also actively investing for the future. When it comes to people, we are developing an environment where employees feel a sense of purpose in their work. Key initiatives include support programs for veteran employees under the policy of creating an environment for continued employment until age 70, the Future Management School (Lite) training program to foster career awareness among female employees as part of our diversity efforts, and Career Vision Dialogues to support long-term career development.

In the area of AI, we plan to actively invest in IT platforms and digital transformation (DX) initiatives with the aim of enhancing our competitiveness through advanced AI utilization. As for local investment, we established a new Regional Revitalization Office in April 2025. Centered around a cycling project, this office is tasked with promoting regional economic revitalization, and we have allocated additional budget and personnel to support these efforts.

The third policy is “Toward an Exciting Future Beyond a Brighter Suruga.” As mentioned earlier, “excitement” comes from within—it stems from having a sense of mission and values that resonate with your work. When your job aligns with those values, it brings enjoyment, emotional engagement, and even moments of joy when customers express their appreciation. By embracing the challenge of creating “difference,” we aim to earn those words, “I’m glad we met.” And when that cycle takes hold, it creates true excitement. That is the vision we are striving for.

One employee once said to me, “It’s true that Suruga has become a brighter place. But when I joined, I believed Suruga Bank was the best. Things have improved, but we’re not the best yet.” Hearing that reminded me that it’s not enough to be satisfied with getting better—we must aim to be the best.

But what kind of “best” are we aiming for? It’s not about size. Even if we remain small, I want us to be a bank where our people proudly talk about what makes us different—and where everyone feels that “when it comes to excitement, it’s Suruga.”

Our Partnership with Credit Saison Moves to the Next Stage

Our capital and business alliance with Credit Saison, launched in 2023, has been progressing smoothly thanks to the complementary strengths of both companies’ sales networks and talent. As of the end of fiscal 2024, cumulative results include ¥22.5 billion in housing loans executed by Suruga, ¥61.2 billion in real estate finance, and over 3,800 credit cards issued. We anticipate that these results will continue to exceed expectations in fiscal 2025.

Even in a world with interest rates, we see this alliance with Credit Saison as one of our key strengths, and we now aim to take our partnership to the next stage. In the first stage, the two companies worked together to offer complementary products and services to new customers. In the second stage, we plan to focus on customers who already do business with both companies, especially in the payments space. The goal is to deliver seamless solutions and work together to expand sticky deposits—deposits that remain with us for the long term.

Some of the ideas currently under consideration include a service allowing customers to convert Credit Saison’s Permanent Points into deposits in their Suruga Bank accounts, and a feature that lets users check their Suruga account balance via the Credit Saison smartphone app. By integrating Saison Cards and Suruga accounts into a seamless experience, we aim to improve convenience and encourage more active use of payment services. On top of that, we hope to further combine these offerings with other banking services, such as time deposits and investment trusts, to deliver new and meaningful experiences to our customers through a truly unified approach.

Expanding Human Capital Investment to Drive Sustainable Growth

One of our key management policies for fiscal 2025 is investment in people, in other words, human capital investment. While our strong performance is certainly encouraging, it has also made it increasingly clear that securing the talent needed to support growth is a critical management issue across all functions—front office, middle office, and back office alike. We currently have around 20 secondees from Credit Saison supporting our operations, yet the need for additional personnel remains pressing.

We do not view human capital investment as an expense, but as a strategic investment for sustainable growth, and as such, we will continue to expand it. Our support programs for veteran employees are becoming well established within the company, with 68 employees already officially recognized under the program. In addition, we are actively promoting mid-career hiring, including a comeback program for former employees. We also plan to raise the starting salary for new hires from fiscal 2026 to a maximum of ¥280,000 per month in order to further strengthen recruitment.

Following the increase implemented in fiscal 2024, we will again raise base salaries in fiscal 2025. The average salary increase for general employees, including bonus enhancements, will be 7%. We will also raise base salaries for Associate Staff (AS), our general administrative employees, and increase hourly wages for Career Staff (CS), our part-time employees. These measures reflect our commitment to rewarding our people for their contributions.

Reviving Overseas IR Activities to Enhance Shareholder Value

In May 2025, we received a request for a report from Japan’s Financial Services Agency (FSA) regarding irregularities in real estate investment loans, excluding share house loans, issued in or prior to 2018 (the “Apaman Issue”). We sincerely apologize to the affected borrowers, as well as to our shareholders and other stakeholders, for the inconvenience and concern this matter has caused.

We take this request from the FSA very seriously. Suruga Bank is committed to addressing each borrower’s unique circumstances with care and compassion, and to doing our utmost to dispel concerns among all stakeholders. We are also working to accelerate resolution on a case-by-case basis, and would like to take this opportunity to report these efforts.

To enhance shareholder value and strengthen our governance, we have already focused heavily on strategic investor relations (IR) activities and more robust disclosure. As part of our renewed commitment to deeper dialogue with shareholders, we plan to resume overseas IR activities in the fall of 2025, something we have not conducted in recent years.

Since the improper lending issue involving share houses, interest from overseas investors had declined significantly. However, we are now seeing renewed interest, and with our share price on an upward trajectory, I believe it is more important than ever to actively engage in dialogue and broaden our base of long-term overseas investors.

Suruga Bank is experiencing a faster-than-expected V-shaped recovery and is now firmly on a path of strong regrowth. The driving force behind this progress is, without a doubt, our employees. It is my role to create an environment where they can approach their work with a strong sense of mission and maintain a sense of excitement. I look forward to continuing conversations about what that excitement means to each of us as we shape the next Mid-Term Management Plan, set to begin in fiscal 2026.

While the future remains uncertain, we will not stand still. We will move forward in directions that our employees find stimulating and exciting—and learn as we go.

To all our stakeholders, we sincerely appreciate your continued understanding and support.

The ceiling represents the bottom of a Black Ship. It was designed with the hope that people would discuss the spirit of enterprise, which can be called the origin of Suruga's DNA, in this free space.

Note : This document has been translated from the Japanese original for reference purposes only.

In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail.